The post-Egypt, in-medias-res-Libya oil spikes, combined with slow, but semi-sustainable economic recovery in the U.S. and Western Europe, plus the continuously surging (on paper) Chinese juggernaut, has brought Peak Oil back to people's lips.

But, should we really be talking about "Peak Commodities"? Possibly. Copper prices, and thefts, are rising again. Even if only a small portion of U.S. agricultural problems are due to climate change, that's more than zero.

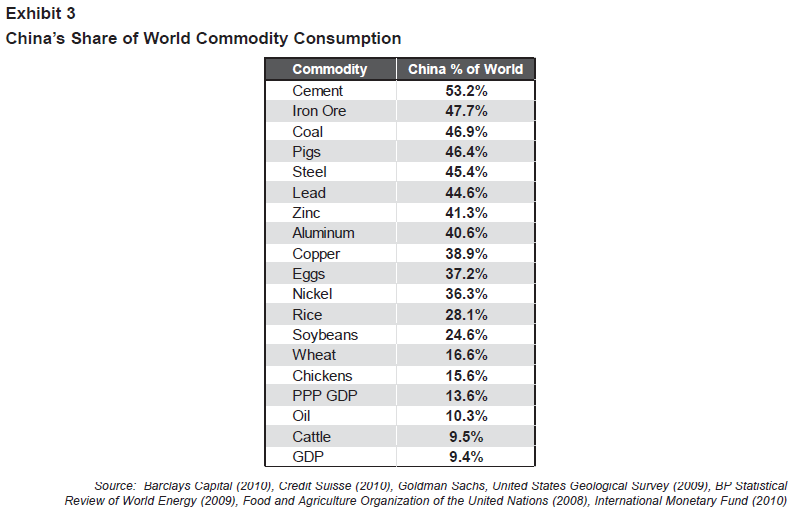

And, as Japan definitely knows, China has a few commodities in its possession and can squeeze the taps.

Beyond that, Beijing is voracious with many items, perhaps due in part to inefficiencies.

And, those inefficiences mean that, if China stumbles, we can see international price bubbles:

Quite separately, several of my smart colleagues agree with Jim Chanos that China’s structural imbalances will cause at least one wheel to come off of their economy within the next 12 months. This is painful when traveling at warp speed – 10% a year in GDP growth. The litany of problems is as follows:The wage inflation, if combined with even more surge in oil prices, won't mean new manufacturing jobs in the U.S., at least not many.

a) An unprecedented rise in wages has reduced China’s competitive strength.

b) The remarkable 50% of GDP going into capital spending was partly the result of a heroic and desperate effort to keep the ship afloat as the Western banking system collapsed. It cannot be sustained, and much of the spending is likely to have been wasted: unnecessary airports, roads, and railroads and unoccupied high-rise apartments.

c) Debt levels have grown much too fast.

d) House prices are deep into bubble territory and there is an unknown, though likely large, quantity of bad loans.

You have heard it all better and in more detail from both Edward Chancellor and Jim Chanos. The significance here is that given China’s overwhelming influence on so many commodities, especially in terms of the percentage China represents of new growth in global demand, any general economic stutter in China can mean very big declines in some of their prices.

It will, though, as I've said before, mean many new manufacturing jobs in Mexico. That could help its economy and stabilize the U.S.-Mexico border ... if ...

If Mexico can get reasonable oil supplies of its own.

No comments:

Post a Comment